The views expressed here do not reflect those of the Federal Reserve Board or the Federal Reserve System.

Publications

What Hundreds of Economic News Events Say About Belief Overreaction in the Stock Market, forthcoming at Review of Financial Studies

with Francesco Bianchi (Johns Hopkins) and Sydney C. Ludvigson (NYU)

The Financial Channel of the Exchange Rate and Global Trade, forthcoming at Review of Financial Studies

with Tim Schmidt-Eisenlohr (FRB)

The Global Transmission of Real Economic Uncertainty

with Juan M. Londono (FRB) and Beth Anne Wilson (FRB)

Journal of Money, Credit and Banking, Volume 57(5), August 2025, Pages 1103-1133

Housing Risk and the Cross-Section of Returns Across Many Asset Classes

with Shaojun Zhang (OSU Fisher)

Real Estate Economics, Volume 53(2), March 2025, Pages 326-351

Housing Cycles and Exchange Rates (Appendix)

with Shaojun Zhang (OSU Fisher)

Management Science, Volume 70(9), September 2024, Pages 5627-6482

Review of Economic Dynamics, Volume 50, October 2023, Pages 211-234

What is Certain about Uncertainty (A survey on uncertainty measures)

Journal of Economic Literature, Vol 61 (2), June 2023

Co-author list (All from FRB): Danilo Cascaldi-Garcia, Cisil Sarisoy, Juan M. Londono, John H. Rogers, Bo Sun, Deepa Datta, Thiago R.T. Ferreira, Olesya V. Grishchenko, Mohammad R. Jahan-Parvar, Francesca Loria, Marius Rodriguez, Ilknur Z

with Boyan Jovanovic (NYU) and Peter L. Rousseau (Vanderbilt)

Journal of Economic Growth, Vol 27 (3), September 2022, pp. 315–363

Belief Distortions and Macroeconomic Fluctuations

with Francesco Bianchi (Johns Hopkins) and Sydney C. Ludvigson (NYU)

American Economic Review, Vol 112, No.7, July 2022, pp. 2269-2315

Uncertainty and Growth Disasters

Review of Economic Dynamics, Volume 44, April 2022, Pages 33-64

Uncertainty and Business Cycles: Exogenous Impulse or Endogenous Response?

with Sydney C. Ludvigson (NYU) and Serena Ng (Columbia)

AEJ: Macro 13 (4), October 2021, pp. 369-410.

Macro and Financial Uncertainty Index (Updated every February and August) Last Update: 2025 August

COVID19 and The Costs of Deadly Disasters

with Sydney C. Ludvigson (NYU) and Serena Ng (Columbia)

AEA Papers and Proceedings 111, May 2021, pp 366-370

The version published in CEPR COVID Economics Issue 9. NBER Working Paper No. 26987

Capital Share Risk in U.S. Asset Pricing (Appendix)

with Martin Lettau (Berkeley Hass) and Sydney C. Ludvigson (NYU)

Journal of Finance 74(4), August 2019, pp. 1753-1792.

Fed Policy Papers/Notes

Downside and Upside Economic Uncertainty (Juan M. Londono), FEDS Notes, February 2026

Risk and Uncertainty in a Post-Pandemic World (Juan M. Londono and Ilknur Zer), FEDS Notes, July 2025

Costs of Rising Uncertainty (Juan M. Londono and Beth Anne Wilson), FEDS Notes, April 2025

The Global Transmission of Inflation Uncertainty (Juan M. Londono and Thomas Li), FEDS Notes, January 2025

Global Inflation Uncertainty and its Economic Effects (Juan M. Londono and Beth Anne Wilson), FEDS Notes, September 2023

Global Real Economic Uncertainty and COVID-19 (Ranie Lin and Juan M. Londono), FEDS Notes, February 2022

Quantifying the Impact of Foreign Economic Uncertainty on the U.S. Economy (Juan M. Londono and Beth Anne Wilson), FEDS Notes, October 2019

Working Papers

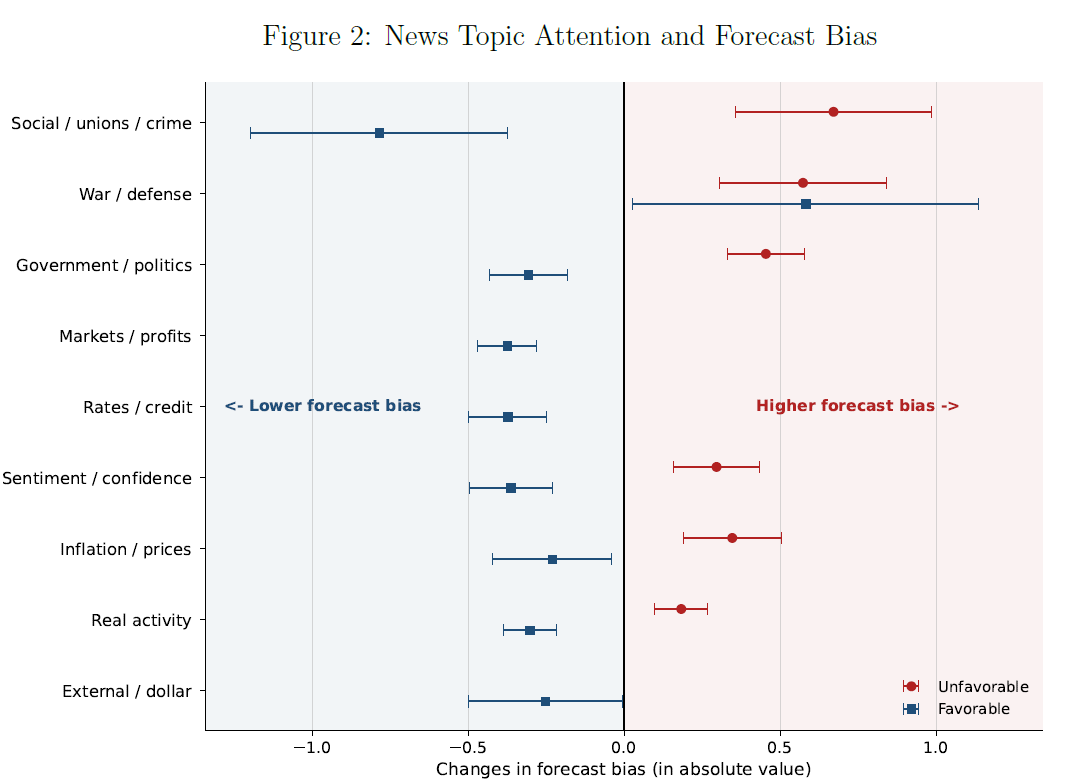

Attention Allocation and Belief Distortion (June 2026)

The specific content and sentiment of the news households process directly dictates their inflation forecast bias.

A Model of Polarization (June 2026), Under R&R at Theoretical Economics

Learning Curves and Organizational Memory (March 2026)

Transmission Growth-at-Risk (March 2026)

with Viktors Stebunovs (FRB) and Judit Temesvary (FRB)

Dissecting Trade Uncertainty (January 2026) Slides

with Juan M. Londono (FRB) and Sophia Qin (Stanford)

The Unseen Cost of Inflation: Measuring Inflation Uncertainty and Its Economic Repercussions (January 2026)

with Juan M. Londono (FRB) and Beth Anne Wilson (FRB)

The Prestakes of Stock Market Investing (Oct 2025)

with Francesco Bianchi (Johns Hopkins), Do Lee (NYU), Sydney C. Ludvigson (NYU)

U.S. Real Economic Uncertainty and the International Stock Market: GVAR Approach (May 2025), with Tony Sun (FRB)

A Structural Approach to High-Frequency Event Studies: The Fed and Markets as Case History (April 2025)

with Francesco Bianchi (Johns Hopkins) and Sydney C. Ludvigson (NYU)

Heterogeneous Intermediaries and Asset Prices: A Semiparametric Approach (July 2024), Under R&R at JFQA

An updated and streamlined version of my JMP (2018)

Shock Restricted Structural Vector-Autoregressions (Jan. 2020, Slides for AEA2020)

with Sydney C. Ludvigson (NYU) and Serena Ng (Columbia)

NBER Working Paper No. 23225

Selected Work in Progress/Major Revisions

Momentum Undervalue Puzzle (with Sydney Ludvigson and Martin Lettau)

Competition and Implementation Cycles

Asset Prices and Dynamic Intermediation Chains in OTC Markets

The Causal Effect of the Dollar on Trade Price with Tim Schmidt-Eisenlohr (FRB) and Shaojun Zhang (OSU Fisher)